October 2011

Beginner

442 pages

11h 49m

English

When a seller receives only part of the sales price during the year of sale, the seller may elect to report the gain on an installment sale basis. The potential for an installment sale occurs when the seller carries paper, that is, as part of the purchase price the seller agrees to hold a mortgage.

If the seller does not receive all of the sale proceeds in the year of sale, then the gain may be spread, on a pro rata basis, over the term of the installment sale.

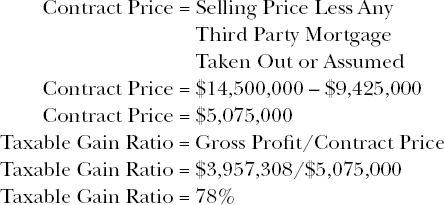

Let us assume that when Jack sells to Stable, the financing market is so tight that he is able to secure only a first trust deed of 65 percent LTV, or $$9,425,000. Stable puts down 25 percent, or $3,625,000, but based on the size of the first mortgage, there is still a gap of $1,450,000. In order to close this gap, Diamond Jack agrees to take back the remaining balance in the form of a note payable $290,000 per year for the next five years. The amount that must be reported annually is determined by a ratio between the gross profit and the contract price. This ratio is called the “Taxable Gain Ratio.”

The gross profit was calculated above as $3,957,308. The contract price equals the selling price less the balance of any mortgage payable by the buyer to a third party. The contract price equals $5,075,000, as shown below.

The result is that 78 percent of the sales proceeds equals the taxable gain. Hence, every ...

Read now

Unlock full access