April 2018

Beginner to intermediate

500 pages

11h 26m

English

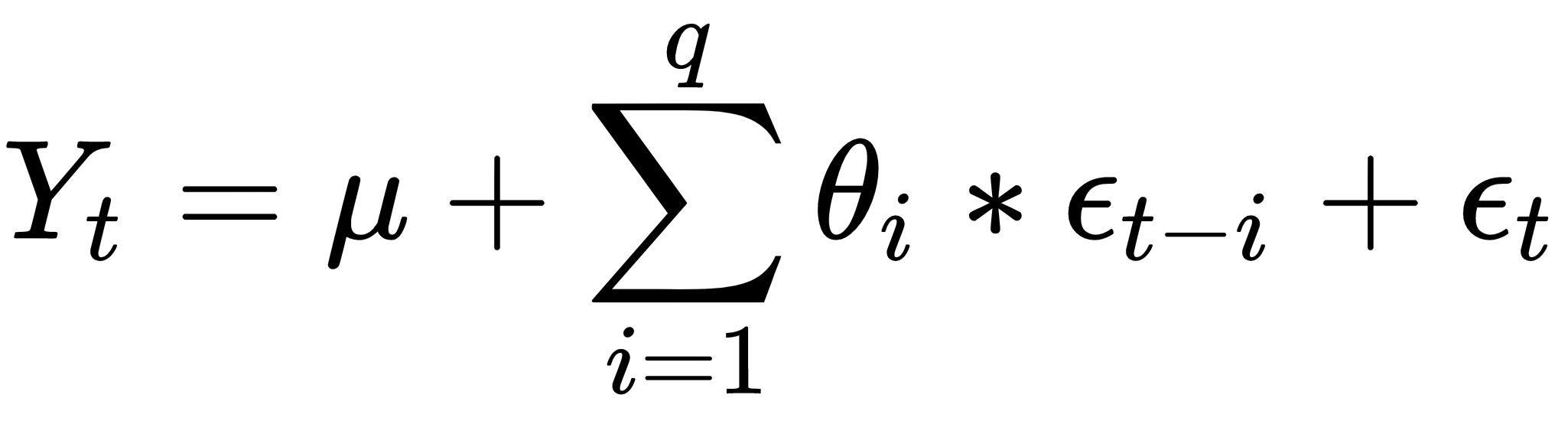

The MA model specifies that the output variable depends linearly on the past and current past values of a stochastic term (imperfectly predictable). The MA model should not be confused with the MA we have seen in the previous sections. This is an essentially different concept although some similarities are evident. Unlike the AR model, the finished MA model is always stationary.

Just as a model AR (p) regresses with respect to the past values of the series, an MA (q) model uses past errors as explanatory variables.

The MA model of q order is defined as:

In the previous formula, the terms are defined as follows:

Read now

Unlock full access