RECEIVE FIXED & PAY FLOATING—ILLUSTRATION 1

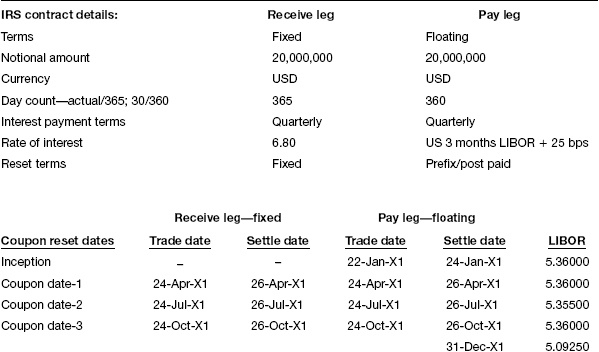

Table 7.2 Details of the interest rate swap contract

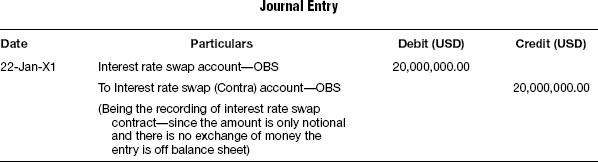

Recording the trade—contingent (at the inception of the interest rate swap)

Unlike bonds and equities, in an interest rate swap generally there is no exchange of money taking place of principal during the purchase or at the maturity of the swap. The interest rates to be paid are calculated on a notional amount.

In the current example, fixed interest is receivable on the notional principal and a floating interest is payable based on 3 LIBOR + 25 basis points. This interest rate swap agreement is based on “fixed-for-floating,” a series of payments calculated by applying a fixed rate of interest to a notional principal amount in exchange for a stream of payments similarly calculated but using a floating rate of interest.

As this is a notional amount and no physical exchange of money takes place, an off balance sheet entry as shown in Table 7.3 is made to record the transaction.

Table 7.3 On purchase of interest rate swap trade

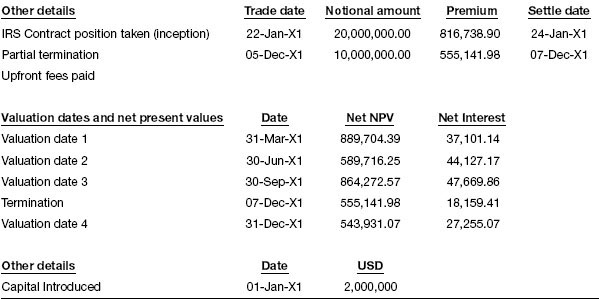

Account for the upfront fee at the inception of an interest rate swap trade

The net present value of the trade at the time of entering into the contract is also known ...

Get Accounting for Investments, Volume 2: Fixed Income Securities and Interest Rate Derivatives—A Practitioner's Guide now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.