September 2017

Beginner to intermediate

560 pages

25h 18m

English

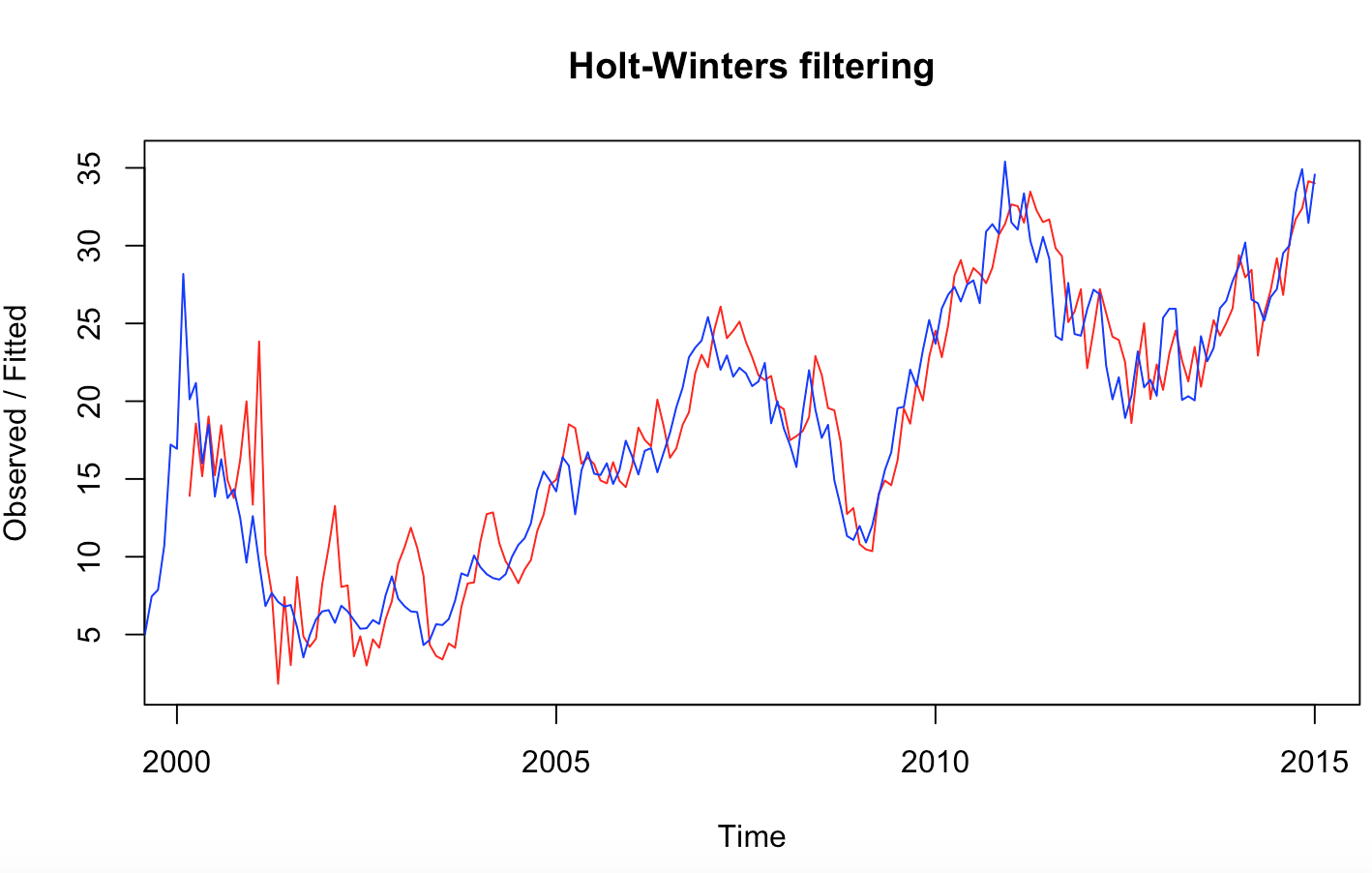

To apply the HoltWinters method for exponential smoothing and forecasting, follow these steps:

> infy <- read.csv("infy-monthly.csv")

> infy.ts <- ts(infy$Adj.Close, start = c(1999,3), frequency = 12)

> infy.hw <- HoltWinters(infy.ts)

> plot(infy.hw, col = "blue", col.predicted = "red")

The plotted result can be seen as follows:

> # See the squared errors > infy.hw$SSE [1] 1446.232 > ...

Read now

Unlock full access