THE COMPLETE STATEMENT OF CASH FLOWS

We have now derived the cash flows of the period and can prepare the statement of cash flows. The following sections cover the direct method and the indirect method.

The Direct Method

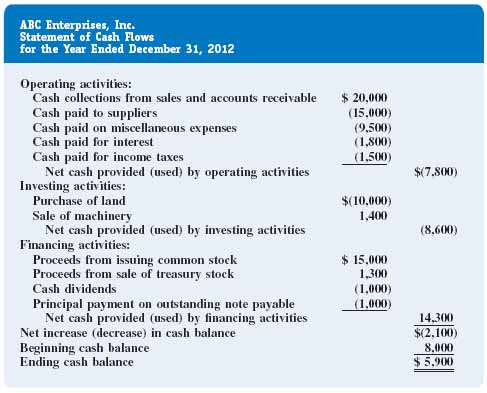

A statement of cash flows prepared under the direct method is provided in Figure 14-18. Note that the dollar amounts are identical to the cash flows derived in the previous section.

FIGURE 14-18 Statement of cash flows for ABC Enterprises: Direct method

![]() Note that cash outflows due to interest are disclosed in the operating section under U.S. GAAP. Under IFRS, firms can choose to disclose interest in the operating or financing sections.

Note that cash outflows due to interest are disclosed in the operating section under U.S. GAAP. Under IFRS, firms can choose to disclose interest in the operating or financing sections.

The Indirect Method

The statement of cash flows under the indirect method is exactly the same as the direct method, except for the presentation of the operating section and the derivation of net cash provided (used) by operating activities. The operating section presented under the indirect method for ABC Enterprises, Inc. is illustrated in Figure 14-19. Note first that the dollar amount of net cash provided (used) by operating activities is the same (—$7,800) whether the direct or the indirect method is used. The difference is in the way in which the amount is computed. Under the indirect method, net cash provided by operating activities ...

Get Financial Accounting: In an Economic Context now with the O’Reilly learning platform.

O’Reilly members experience books, live events, courses curated by job role, and more from O’Reilly and nearly 200 top publishers.