December 2018

Beginner to intermediate

684 pages

21h 9m

English

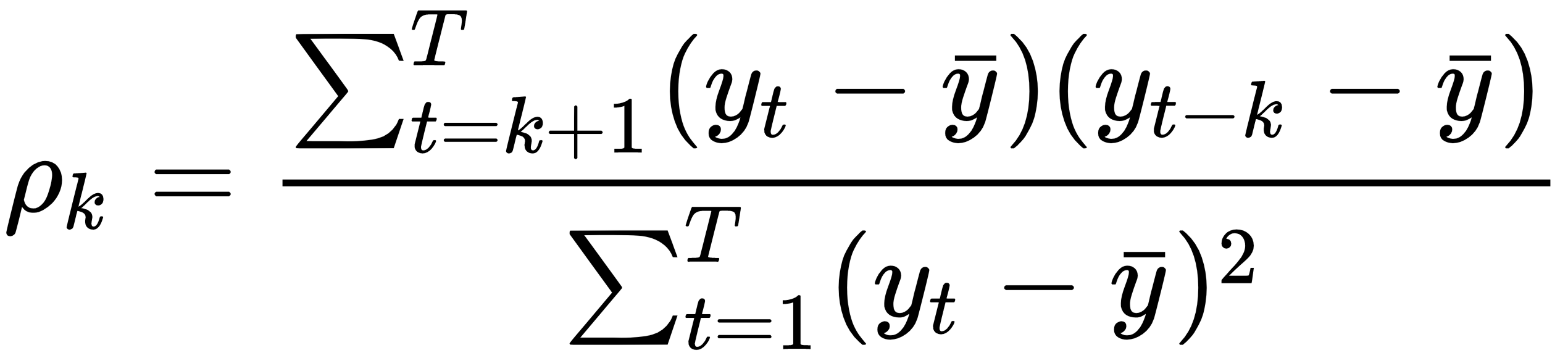

Autocorrelation (also called serial correlation) adapts the concept of correlation to the time series context: just as the correlation coefficient measures the strength of a linear relationship between two variables, the autocorrelation coefficient, ρk, measures the extent of a linear relationship between time series values separated by a given lag, k:

Hence, we can calculate one autocorrelation coefficient for each of the T-1 lags in a time series; T is the length of the series. The autocorrelation function (ACF) computes the correlation coefficients as a function of the lag.

The autocorrelation for a lag larger ...